Virtual reality (VR) is an advanced technology that creates immersive, computer-generated environments, enabling users to interact with simulated surroundings in a highly realistic manner. In recent years, VR has gained significant popularity due to its wide range of applications across industries such as gaming, education, healthcare, and entertainment.

Editor Picks

- Global shipments of AR/VR headsets increased by 10% in 2024, reflecting continued growth in consumer and enterprise adoption of immersive technologies.

- Meta maintained its leadership position in the global AR/VR headset market, accounting for 74.6% of total shipments in 2024.

- Apple emerged as the second-largest vendor with a 5.2% market share, followed by Sony with 4.3%, ByteDance with 4.1%, and XREAL with 3.3%, collectively representing the leading players in the AR/VR headset industry.

- According to industry estimates, global AR/VR headset shipments reached 14.3 million units in 2025, representing a significant 39.2% year-over-year increase.

- Global VR headset shipments are projected to exceed 70 million units by 2028, supported by ongoing technological advancements, expanding content ecosystems, and increasing consumer demand.

- The worldwide VR user base is estimated at approximately 171 million users, highlighting the growing adoption of immersive digital experiences across multiple applications.

- In the United States, approximately 53 million adults currently own a VR system, demonstrating substantial market penetration among consumers.

- 8% of U.S. adults who do not currently own a VR device are likely to purchase one within the next six months, potentially adding 14 million new users and contributing to an estimated 21% expansion of the U.S. VR market.

Historical Snapshot

- 2012–2016

- 2012: Oculus Rift DK1 – Kickstarter campaign launches modern VR movement

- 2014: Facebook acquires Oculus – Major investment boosts industry confidence

- 2016: HTC Vive / PlayStation VR – Launch of PC VR with full tracking and mainstream console VR

- 2017–2023

- 2019: Oculus Quest – First successful standalone VR system

- 2020: Half-Life: Alyx – Landmark triple-A VR game release

- 2022: Meta Quest Pro / Pico 4 – Advanced standalone headsets for work and consumer use

- 2023: Apple Vision Pro announced – Mainstream tech entry validates mixed reality

- 2024–2026

- 2024: Advanced haptics – Integrated suits and gloves in mainstream applications

- 2025: Cloud Rendering VR – Ultra-realistic graphics via network stream

- 2026: AR/VR Convergence – Sleek eyeglasses blend digital and physical worlds for daily life

Virtual Reality (VR) Market Highlights

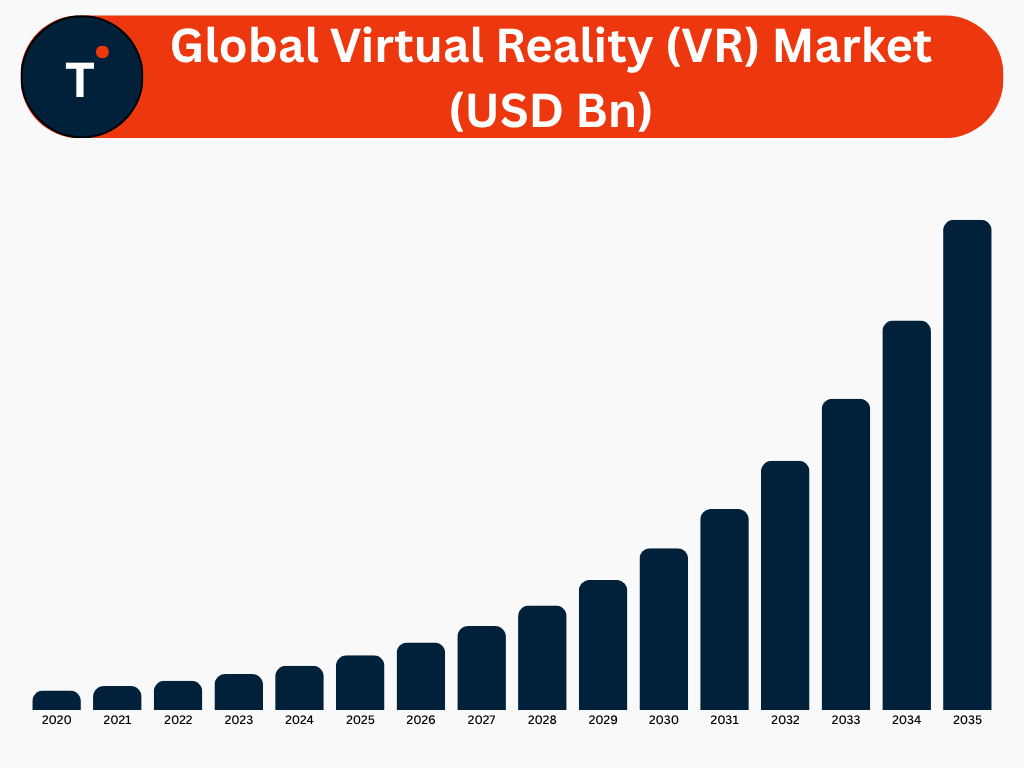

The global virtual reality (VR) market is projected to grow from US$78.20 billion in 2025 to US$701.50 billion by 2035, registering a robust CAGR of 24.6% during the forecast period.

Regional Insights

- North America accounted for the largest share of the global VR market, capturing 37.0% of total revenue in 2025.

- The North American VR market was valued at US$ 28.96 billion in 2025 and is anticipated to reach US$ 255.33 billion by 2035, expanding at a CAGR of 24.4%.

- Within North America, the United States dominated the regional market with a 92.1% share in 2025.

- The U.S. VR market was valued at US$ 26.67 billion in 2025 and is projected to attain US$ 229.80 billion by 2035, registering a CAGR of 24.1%.

- Asia Pacific emerged as the most lucrative region and accounted for 33.0% of the global market share in 2025.

- The Asia Pacific VR market was valued at US$ 25.80 billion in 2025 and is expected to reach US$ 275.69 billion by 2035, growing at the highest regional CAGR of 26.9%.

- Europe represented 23.8% of the global VR market in 2025.

- The European market was valued at US$ 18.59 billion in 2025 and is forecast to reach US$ 147.57 billion by 2035, registering a CAGR of 23.0%.

- The Middle East & Africa region held a 2.7% market share in 2025.

- The MEA market was valued at US$ 2.08 billion in 2025 and is projected to grow to US$ 10.83 billion by 2035, at a CAGR of 17.9%.

- Latin America accounted for 3.5% of the global VR market in 2025.

- The market in Latin America was valued at US$ 2.76 billion in 2025 and is anticipated to reach US$ 12.07 billion by 2035, expanding at a CAGR of 15.9% during the forecast period.

Segment Insights

By Component

- The hardware segment dominated the global VR market, accounting for 63.8% of total revenue in 2025.

- The segment was valued at US$ 49.87 billion in 2025 and is expected to reach US$ 401.88 billion by 2035, registering a CAGR of 23.3%.

By Technology

- The semi-immersive and fully immersive technology segment held the largest market share of 91.6% in 2025.

- The segment was valued at US$ 71.66 billion in 2025 and is projected to reach US$ 673.91 billion by 2035, growing at a CAGR of 25.2%.

By Device Type

- The Head-Mounted Display (HMD) segment dominated the market with a 71.3% share in 2025.

- The segment generated revenues of US$ 55.75 billion in 2025 and is expected to reach US$ 488.11 billion by 2035, expanding at a CAGR of 24.3%.

By End Use

- The gaming sector represented the leading end-use segment, accounting for 32.0% of the global market share in 2025.

- The segment was valued at US$ 25.05 billion in 2025 and is projected to reach US$ 259.01 billion by 2035, registering a CAGR of 26.2% over the forecast period.

Virtual Reality (VR) Adoption and User Engagement Insights

- Approximately 55% of virtual reality users report satisfaction with their overall VR experience, indicating positive consumer perception and acceptance of the technology.

- The implementation of virtual reality in workplace training and operational environments has been shown to reduce the risk of workplace injuries by up to 43%, highlighting its value in safety-focused applications.

- VR engagement levels remain strong, with 88% of headset owners using their devices several times per month, while 60% report using VR more than once per week.

- Around 60% of VR users indicate that they retain information more effectively when learning through virtual reality compared to traditional learning methods, demonstrating VR’s potential as an educational and training tool.

- Approximately 80% of users report higher levels of engagement with VR content than with conventional two-dimensional (2D) content, underscoring the immersive nature of the technology.

- Nearly 70% of VR users state that they would recommend virtual reality experiences to others, reflecting strong user advocacy and satisfaction.

- The average VR user spends approximately 20 minutes per session within virtual environments, indicating consistent engagement across applications.

- Studies suggest that users spend three times longer interacting with VR content compared to traditional 2D content, highlighting the technology’s ability to sustain user attention.

- Male users currently represent the majority of the VR user base, accounting for 60% of total users.

- Female users constitute 40% of the VR market, highlighting a growing and increasingly significant presence within the virtual reality ecosystem.

- Employees trained using virtual reality demonstrate significantly improved concentration levels, being four times more focused than online learners and 1.5 times more focused than participants in traditional classroom-based training programs.

- In healthcare applications, surgeons trained through virtual reality simulations have been shown to perform procedures 29% faster and commit six times fewer errors than those who did not receive VR-based training.

- The integration of virtual reality (VR) technologies in e-commerce platforms has been shown to increase online shopping conversion rates by approximately 17%.

- Corporate adoption of virtual reality continues to increase, with 51% of organizations either actively integrating VR into their business strategies or already utilizing the technology within at least one specialized business function.

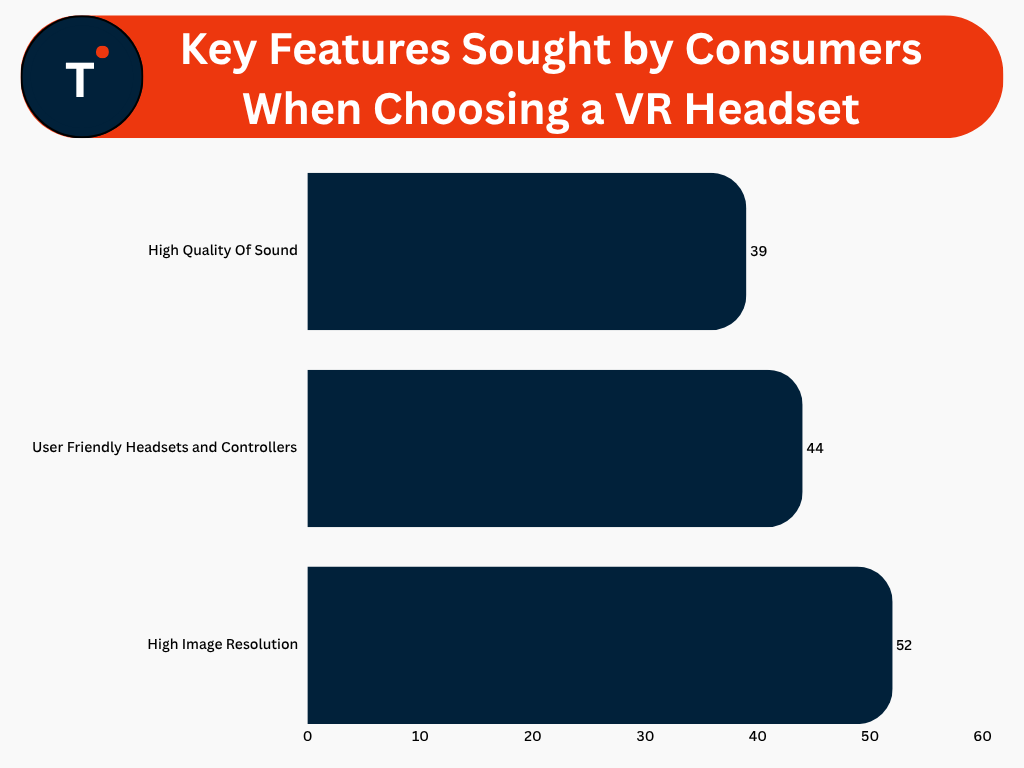

Key Features Sought by Consumers When Choosing a VR Headset:

- A significant 41% of VR gamers prefer engaging in virtual reality experiences with friends or family.

- Approximately 38% of VR gamers favor independent gameplay experiences within virtual environments.

- Around 21% of VR gamers participate in both solo and multiplayer VR experiences, reflecting diverse gameplay preferences.

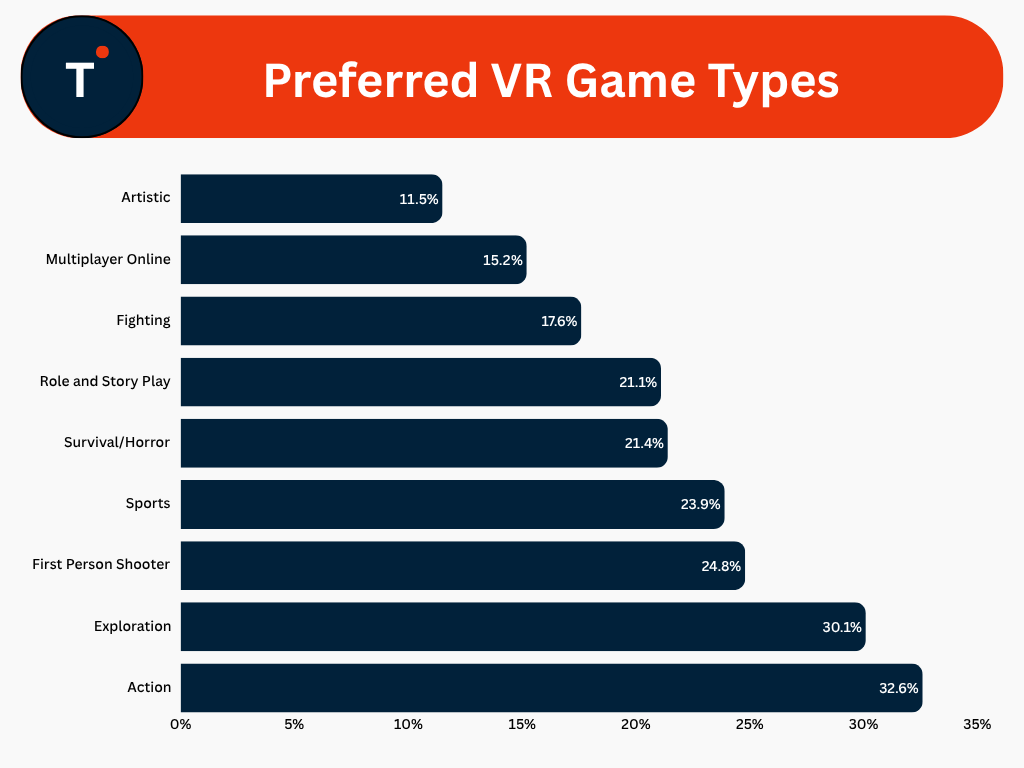

Preferred VR Game Types:

- Across 83 schools within the Inspired Education Group that have implemented immersive technologies in the classroom, 90% of students reported increased engagement and interest in their lessons.

- The use of virtual and mixed reality technologies contributed to a 25% increase in students’ confidence in their subject knowledge, highlighting the effectiveness of immersive learning environments.

- Approximately 85% of teachers identified virtual and mixed reality as valuable tools for enhancing teaching effectiveness and classroom instruction.

- Students utilizing immersive learning technologies demonstrated a 15% improvement in academic performance on multiple-choice assessments.

VR Industry Employee Training and Workforce Benefits

- The adoption of virtual reality technologies is expected to expand significantly, with an estimated 23 million jobs utilizing VR by 2030.

- Virtual reality-based training programs enable employees to complete training courses up to four times faster compared to conventional training methods.

Time to complete training:

| Time to complete training | Minutes |

| Classroom | 120 |

| VR | 29 |

| E-learn | 45 |

- The integration of VR into educational and training programs has been shown to reduce course dropout rates by approximately 30%, improving learner engagement and completion rates.

- VR-based learning delivers substantially higher knowledge retention, achieving a 75% retention rate, compared to traditional lectures (5%), reading-based learning (10%), and audio-visual instruction (20%).

- Approximately 70% of professionals believe that virtual reality will play a significant role in employee training and workforce development across organizations and industries.

Consumer Behavior Analysis

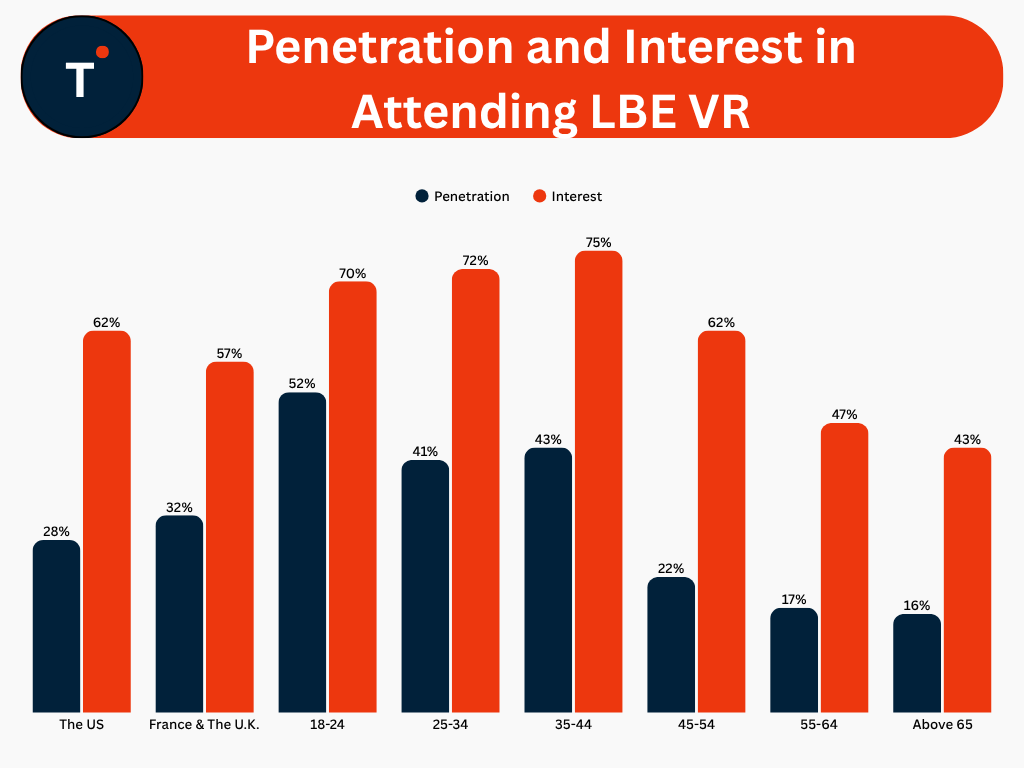

Location-based entertainment virtual reality (LBE VR) continues to demonstrate strong market resilience and sustained growth momentum, reflecting increasing consumer interest in immersive entertainment experiences.

- In the United States, 28% of adults have participated in location-based entertainment (LBE) VR experiences, while 62% express interest in engaging with such experiences.

- Across France and the United Kingdom, LBE VR penetration stands at 32%, with 57% of adults indicating interest in participating.

- Adults aged 18–24 represent a highly engaged demographic, with 52% having experienced LBE VR and 70% expressing interest in future participation.

- Among individuals aged 25–34, 41% have participated in LBE VR experiences, while 72% show interest in engaging with the technology.

- The 35–44 age group demonstrates the highest level of interest, with 75% expressing willingness to participate, while current penetration reaches 43%.

- Adults aged 45–54 exhibit strong latent demand, with 62% expressing interest despite a penetration rate of only 22%.

- Among consumers aged 55–64, participation remains relatively low at 17%, although 47% express interest in LBE VR experiences.

- The 65+ age group records a penetration rate of 16%, while 43% indicate interest in participating in location-based VR experiences.

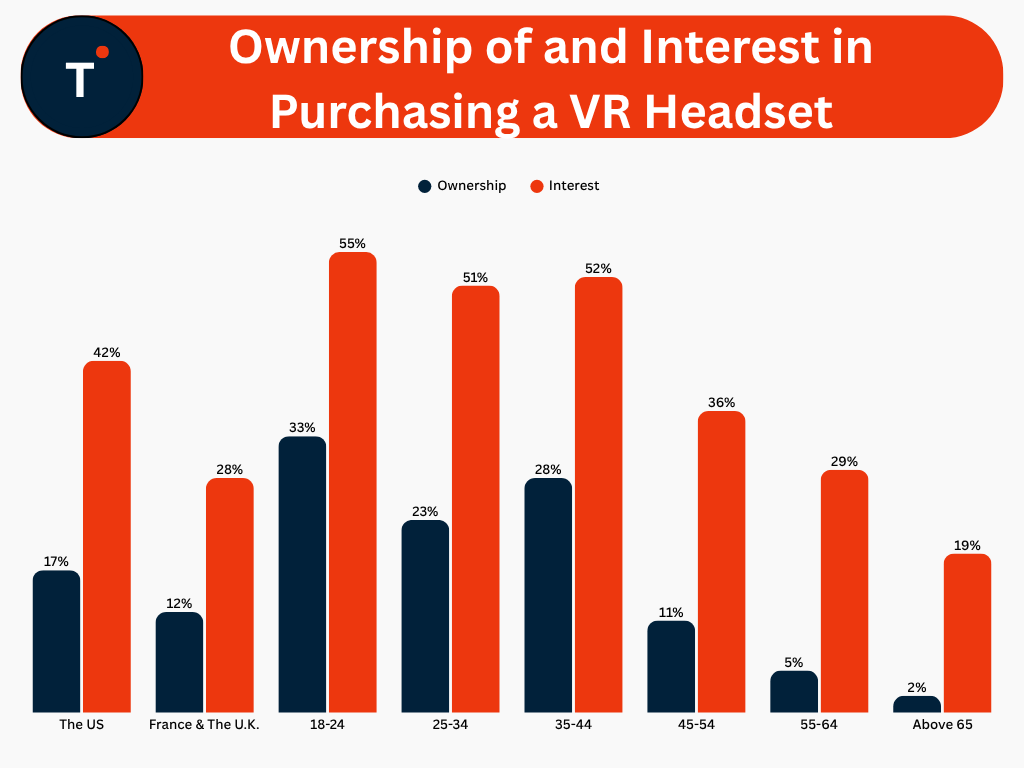

- In the United States, 17% of adults currently own a VR headset, while 42% express interest in purchasing one.

- Across France and the United Kingdom, VR headset ownership stands at 12%, with 28% of adults indicating interest in future purchases.

- Adults aged 18–24 represent the leading consumer segment, with 33% currently owning a VR headset and 55% expressing purchase interest.

- Among individuals aged 25–34, VR headset ownership reaches 23%, while 51% indicate interest in acquiring a device.

- The 35–44 age group records a headset ownership rate of 28%, accompanied by a purchase interest level of 52%.

- Consumers aged 45–54 demonstrate moderate market engagement, with 11% ownership and 36% expressing interest in purchasing a VR headset.

- Among adults aged 55–64, headset ownership remains relatively low at 5%, while 29% express interest in future adoption.

- The 65+ age group exhibits the lowest ownership rate at 2%; however, 19% of consumers within this demographic indicate interest in purchasing a VR headset.

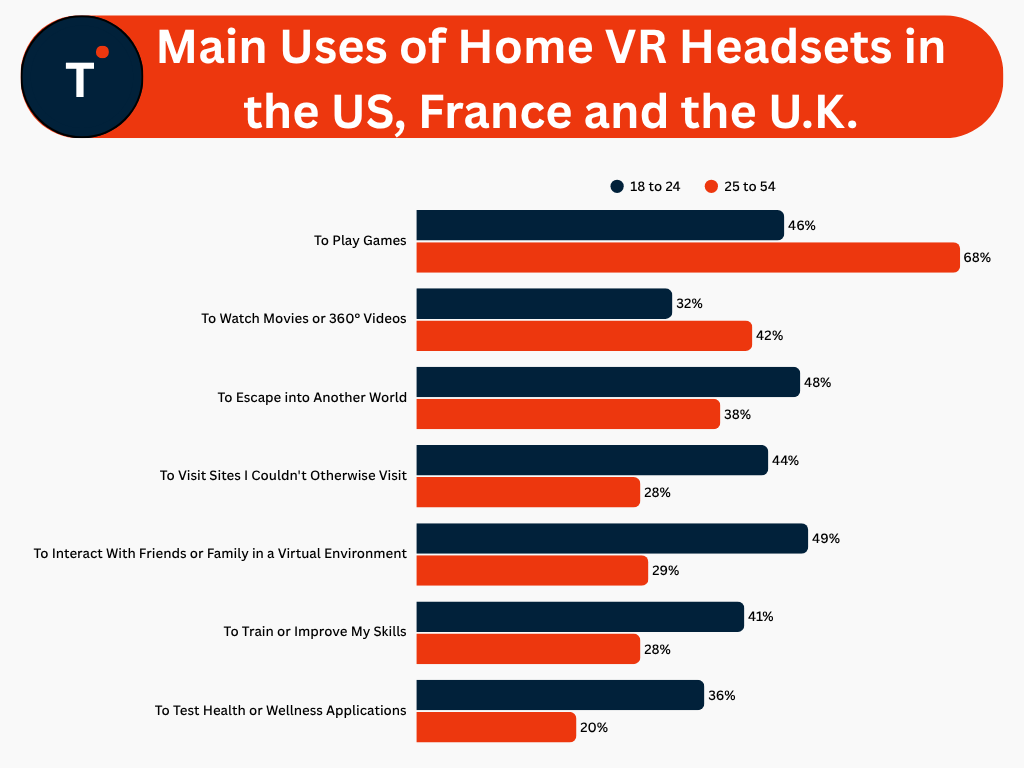

- Gaming is the leading use case among VR headset owners aged 25–54, with 68% using VR for gaming, compared to 46% of users aged 18–24.

- Approximately 42% of VR users aged 25–54 use their headsets to watch movies and 360-degree videos, while 32% of users aged 18–24 engage in this activity.

- Nearly 48% of VR users aged 18–24 utilize VR to experience immersive virtual worlds, compared to 38% of users aged 25–54.

- Virtual tourism is more prevalent among users aged 18–24, with 44% using VR to visit places they could not otherwise experience, compared to 28% of users aged 25–54.

- Social interaction represents a key application among younger users, with 49% of VR headset owners aged 18–24 using VR to interact with friends and family in virtual environments, compared to 29% of users aged 25–54.

- VR-based training and skill development are more common among users aged 18–24, with 41% utilizing VR for educational and training purposes, compared to 28% of users aged 25–54.

- Health and wellness applications are also more widely adopted among users aged 18–24, with 36% using VR for fitness and wellness-related activities, compared to 20% of users aged 25–54.

Investments and Strategic Activity

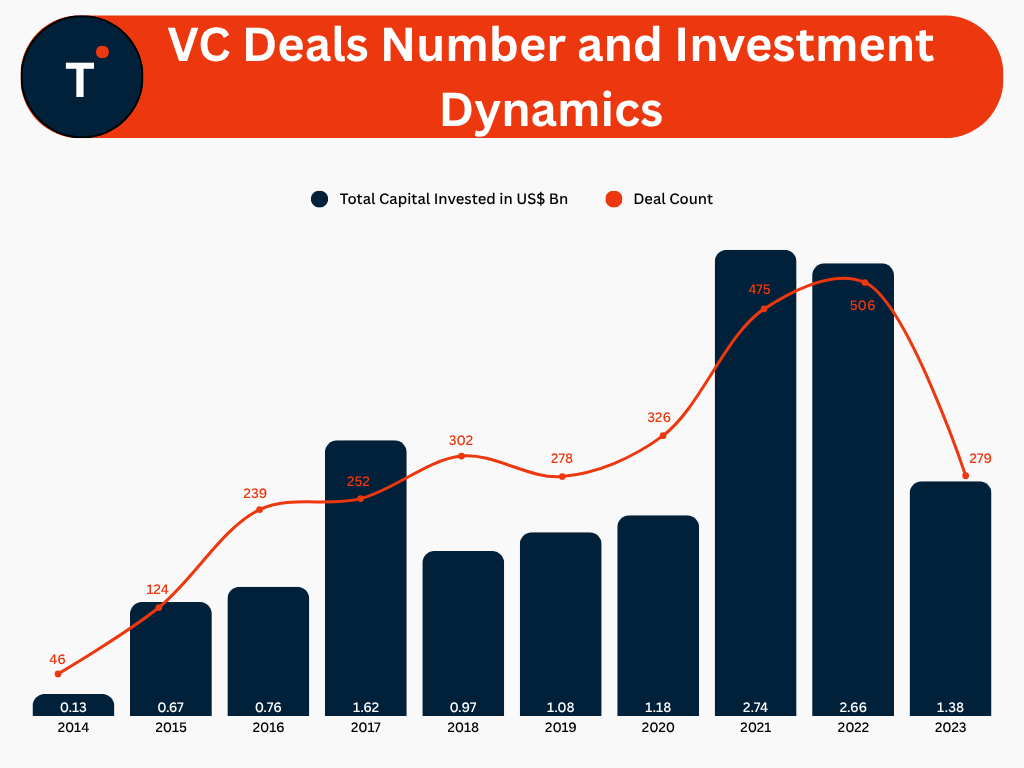

- The virtual reality (VR) industry recorded 279 venture capital deals in 2023, reflecting sustained investor interest in immersive technology solutions.

- Between 2014 and 2023, venture activity in the VR sector expanded at a compound annual growth rate (CAGR) of 22.2%, demonstrating strong long-term investment momentum.

- Venture capital funding in the VR market reached approximately US$ 1.38 billion in 2023, surpassing pre-pandemic investment levels and highlighting renewed confidence in the sector’s growth potential.

- Since 2017, approximately 499 mergers and acquisitions (M&A) transactions have been completed across the virtual reality (VR) and augmented reality (AR) markets.

- Strategic acquisition activity has been led by major technology companies, with Meta, Apple, Snap, Alphabet, and Epic Games emerging as the most active acquirers in the VR/AR ecosystem.

VC Deals Number and Investment Dynamics:

Top Brands and Market Positioning

- Meta’s Oculus product portfolio continues to lead the VR headset market, accounting for nearly half of the installed user base among current VR headset owners.

- During the first three months of 2025, Meta sold approximately 710,000 VR headsets, reinforcing its leadership position despite intensifying market competition.

- Sony’s PlayStation VR2 achieved strong market adoption, surpassing 1 million units sold within its first year of launch.

- The Meta Quest 2 remains one of the most successful VR devices globally, with cumulative sales exceeding 20 million units worldwide.

- Apple Vision Pro generated significant consumer interest, with more than 200,000 pre-orders recorded in the United States during its first month of availability.

- HTC maintains a notable presence within the industry, holding approximately 10% of the global VR market share.

- Pico, a subsidiary of ByteDance, ranks among the leading VR headset manufacturers and currently holds the third position in global VR headset shipments.

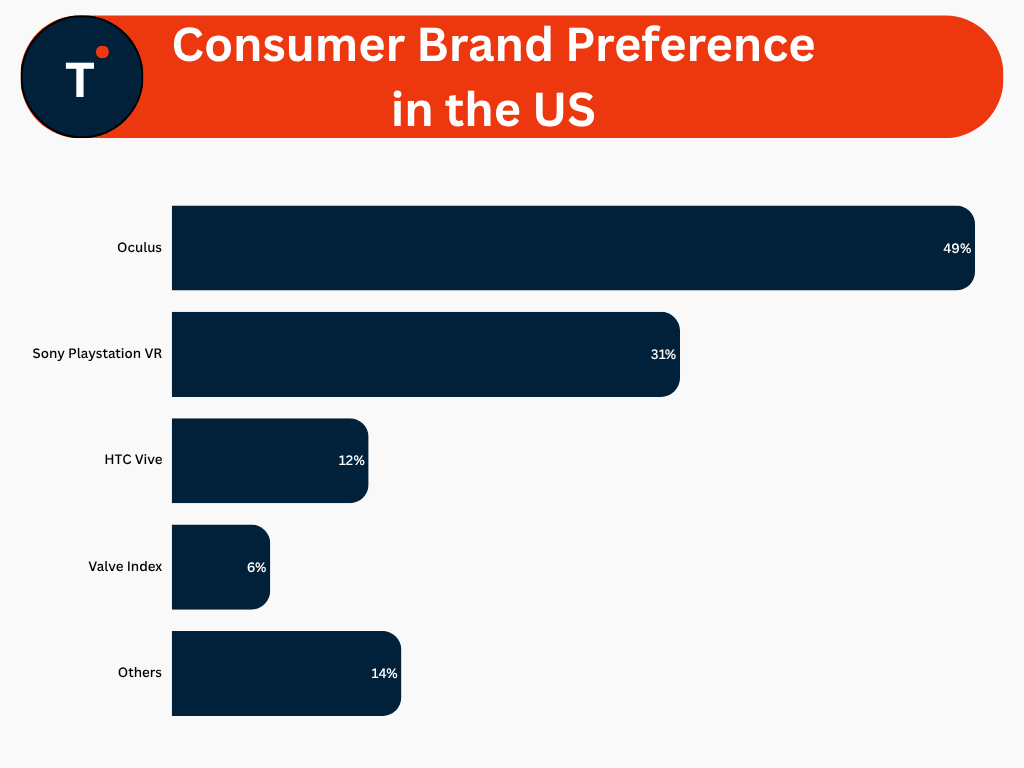

Consumer Brand Preference in the US:

- Oculus is the most preferred VR brand among U.S. consumers, accounting for 49% of brand preference.

- Sony PlayStation VR ranks as the second most preferred VR brand, capturing 31% of consumer preference.

- HTC Vive holds a 12% share of consumer preference, maintaining a notable presence within the U.S. VR market.

- Valve Index accounts for 6% of consumer preference, reflecting a smaller but established user base.

- Other VR brands collectively represent 14% of consumer preference, indicating the presence of several niche and emerging competitors.

- The U.S. VR market remains highly concentrated, with Oculus and Sony PlayStation VR collectively accounting for the majority of consumer brand preference.

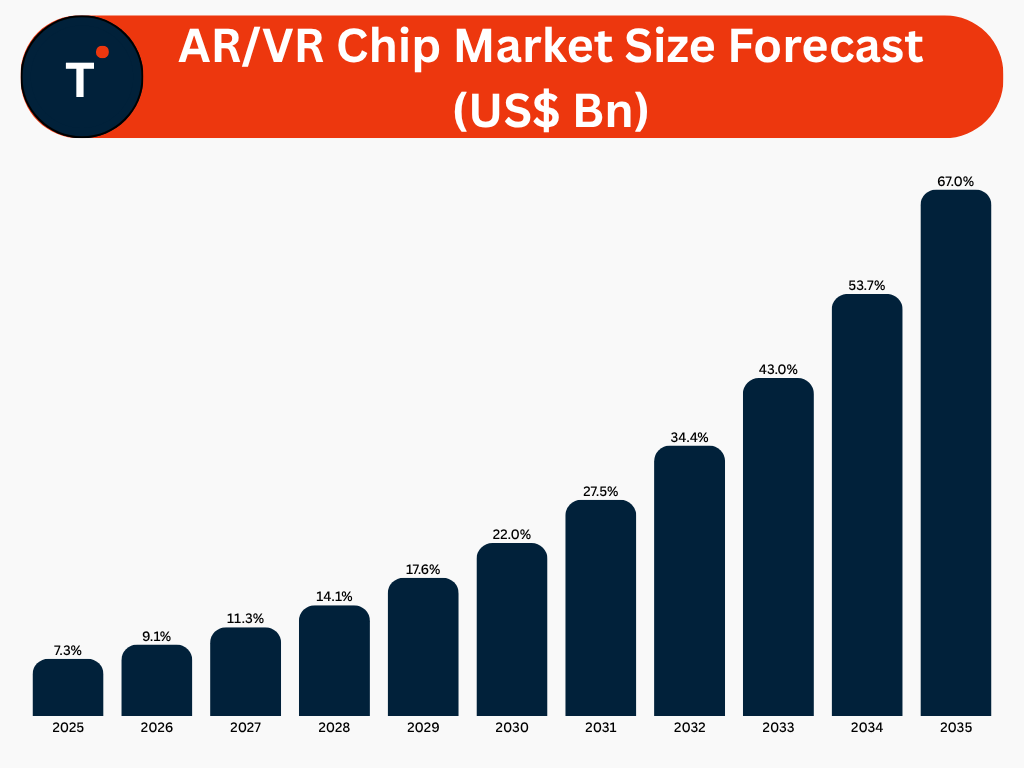

Adjacent Market – AR/VR Chips

- Specialized AR/VR microprocessors have been developed to address the advanced computing and graphics requirements of augmented reality (AR) and virtual reality (VR) applications.

- The AR/VR chip market is primarily led by major semiconductor manufacturers such as Qualcomm and MediaTek, which provide processors optimized for immersive technologies.

- These specialized chips are designed to support the rendering of highly realistic three-dimensional (3D) environments while delivering the low-latency performance necessary for seamless user experiences.

- Advanced AR/VR processors play a critical role in enhancing visual quality, motion tracking accuracy, power efficiency, and real-time responsiveness across immersive devices.

- The growing adoption of AR and VR technologies across gaming, entertainment, healthcare, education, manufacturing, retail, and enterprise applications is driving demand for dedicated AR/VR chipsets.

AR/VR Chip Market Size Forecast (US$ Bn)

Recent Developments

In April 2026, Unity Technologies and Meta expanded their long-standing collaboration through a multi-year platform support and enterprise agreement aimed at strengthening virtual reality development and ecosystem growth.

In May 2026, Sandbox VR announced the opening of a new location at Town Square near the Las Vegas Strip, marking its third venue in Las Vegas and expanding its presence in one of the world’s leading tourism destinations, which attracts more than 40 million visitors annually.

In May 2026, Virtuix Holdings Inc. was selected by the U.S. Air Force for Phase I funding under the AFWERX Small Business Innovation Research (SBIR) program to develop its Virtual Terrain Walk platform for military mission planning applications.

In April 2024, Meta introduced the Meta Quest 3S headset, offering the same mixed reality capabilities and high-performance features as the Meta Quest 3 while targeting a broader consumer base through a more affordable price point.

Affordability and Market Impact

- The average selling price of a high-end virtual reality headset ranged between US$500 and US$1,000 in 2024, reflecting the premium nature of advanced immersive devices.

- Meta Quest 3 entered the market with a starting price of US$499, targeting mainstream consumers seeking advanced mixed reality capabilities.

- Apple Vision Pro was introduced at a premium price point of US$3,499, positioning the device within the high-end spatial computing segment.

- Approximately 65% of consumers identify device cost as the primary barrier to AR/VR adoption, highlighting the importance of affordability in market expansion.

- Entry-level VR devices, such as the Meta Quest 2, are available at approximately US$299, improving accessibility for first-time users.

- AR/VR headset prices have declined by more than 50% since 2016, driven by technological advancements, economies of scale, and increased market competition.

- The cost of AR/VR devices is projected to decrease by approximately 15% annually through 2027, further supporting broader consumer adoption.

- More than 80% of VR users utilize standalone headsets priced below US$600, underscoring the strong demand for affordable and self-contained devices.

- Only 12% of consumers are willing to spend more than US$1,000 on AR/VR hardware, indicating price sensitivity within the consumer market.

- Approximately 45% of enterprises cite hardware costs as a key challenge to AR/VR adoption, particularly for large-scale deployments.

- Around 90% of AR/VR devices sold in 2023 were priced below US$700, demonstrating the market’s preference for mid-range and affordable solutions.

- Educational institutions show a strong preference for AR/VR devices priced below US$400, reflecting budget considerations within the education sector.

- Strategic price reductions contributed to the success of the Meta Quest 2, helping the device achieve cumulative sales exceeding 20 million units.

- Approximately 62% of VR gamers prefer devices priced below US$500, highlighting the importance of competitive pricing in the gaming segment.

- For PC-based VR systems, the cost of a VR-ready computer can add an additional US$800–US$1,200 to the overall setup cost, creating an additional barrier to adoption.

- Enterprise-grade AR/VR solutions can exceed US$5,000 per unit, reflecting the advanced hardware, software, and support requirements of commercial applications.

- Hardware subsidies provided by platform operators and ecosystem providers can reduce consumer purchase prices by up to 25%, improving device accessibility.

- Fewer than 5% of households globally currently own AR/VR devices, with affordability remaining a significant factor limiting widespread adoption.

- Refurbished VR headsets are typically available at 30%–50% below retail pricing, offering a cost-effective alternative for budget-conscious consumers.

- Government procurement programs and institutional bulk purchases can reduce AR/VR device costs by 20%–35%, facilitating adoption across education, healthcare, and public sector organizations.

Conclusion

The global virtual reality market is experiencing rapid growth, driven by advancements in hardware, software, immersive content, and enterprise applications.

North America, led by the United States, remains the largest regional market, supported by strong technology infrastructure, high consumer adoption, significant investments, and the presence of major industry participants.

The Asia-Pacific region is expected to emerge as the fastest-growing market, driven by expanding digitalization, increasing consumer demand, growing gaming communities, and rising investments in immersive technologies.

Increasing adoption across gaming, education, healthcare, retail, manufacturing, and workforce training is expanding the market’s addressable opportunities.

Continuous improvements in device affordability, performance, and user experience are supporting broader consumer and enterprise adoption.

Strong investment activity, strategic partnerships, and ongoing product innovations are accelerating the development of the VR ecosystem.

As adoption continues to broaden across regions and industries, virtual reality is expected to become an integral component of next-generation digital experiences worldwide.