eDiscovery, also known as electronic discovery, involves the identification, collection, and production of electronically stored information (ESI) in response to legal proceedings, investigations, or regulatory requests. Electronically stored information includes emails, documents, presentations, databases, voicemail records, audio and video files, social media content, websites, and other forms of digital data. eDiscovery enables organizations to efficiently locate and produce relevant electronic information while supporting legal and regulatory compliance requirements.

Editor’s Choice

- Global data generation increased from 2 zettabytes in 2010 to 193.68 zettabytes in 2025 and is projected to reach 553 zettabytes by 2029, significantly increasing the volume of electronically stored information requiring management and discovery.

- Corporate data volumes continue to expand rapidly, with more than 80% of enterprise data classified as unstructured or distributed across difficult-to-access data sources, creating growing challenges for legal and compliance teams.

- 42% of law firms reported utilizing artificial intelligence technologies in 2025, compared with 26% in 2024, highlighting the accelerating adoption of AI across legal workflows.

- 42% of legal organizations expect to increase their use of artificial intelligence technologies in 2026 as part of ongoing digital transformation initiatives.

- 46% of legal professionals believe artificial intelligence will have the greatest impact on eDiscovery processes over the next five years, underscoring its growing importance within the legal technology ecosystem.

- Everlaw’s automated coding and review capabilities process 140 documents per hour, delivering performance levels that are 180% faster than the industry average.

- Scalable eDiscovery platforms can reduce the volume of data requiring manual review by up to 80%, significantly improving review efficiency and reducing litigation costs.

- Predictive coding technologies can review up to 50,000 documents per day, compared with the average human review rate of 50 documents per hour, demonstrating substantial productivity advantages.

- Predictive coding solutions achieve an average 95% accuracy rate, exceeding the 70%–80% accuracy levels typically associated with manual document review.

- Research conducted by the RAND Corporation indicates that predictive coding can reduce document review costs by up to 70% in large-scale litigation matters. In cases involving 1 million documents, organizations can realize cost savings exceeding US$2 million.

General Statistics

- AI-assisted document review can deliver cost savings of up to 70% and time savings of up to 80% in large-scale eDiscovery projects, significantly improving operational efficiency.

- Advanced machine learning models achieve document review accuracy rates of up to 95%, outperforming human reviewers, particularly in high-volume and time-sensitive review environments.

- Research conducted by Stanford Law School’s CodeX Center projects that by 2025, AI language models will be capable of understanding and summarizing legal arguments with 95% accuracy, compared with 78% currently achieved.

- AI-powered legal analysis tools are expected to reduce the time required for initial case assessment by up to 70%, enabling legal professionals to focus on strategic decision-making rather than manual document review.

- The integration of knowledge graphs with language models has demonstrated a 40% improvement in identifying relevant case law and statutes compared with traditional keyword-based search methodologies.

- According to the American Bar Association’s Blockchain and Cryptocurrency Committee, 30% of large law firms are expected to adopt blockchain-based eDiscovery systems by 2026, compared with 3% in 2022.

- Blockchain-enabled eDiscovery platforms are projected to reduce data authenticity disputes by 85% and decrease chain-of-custody verification times by 60%, strengthening evidentiary integrity and compliance.

- Gartner forecasts that 70% of eDiscovery platforms will incorporate advanced visual analytics capabilities by 2025, up from 25% in 2022.

- Advanced visual analytics tools are expected to reduce initial data assessment time by 50% while improving the accuracy of relevance determinations by 35%.

- Virtual reality (VR)-based data visualization technologies have demonstrated measurable efficiency gains, with legal professionals completing early case assessments 40% faster through VR-enabled document clustering and relationship mapping tools.

- A consortium of law schools and technology companies is developing a legal-specific large language model (LLM) trained on more than 10 billion words of legal text, supporting more accurate legal analysis and document review.

- Early testing indicates that legal-specific LLMs deliver a 45% improvement in legal task accuracy compared with general-purpose language models.

- Industry analysts project that by 2027, 80% of AmLaw 100 law firms will utilize custom-trained, industry-specific AI models for eDiscovery, compared with 15% in 2023.

- Specialized AI systems trained on patent litigation datasets have demonstrated the ability to predict litigation outcomes with 82% accuracy, supporting more informed intellectual property strategies and case preparation.

- By 2026, AI-powered systems are expected to perform first-pass privilege reviews with 90% accuracy, reducing privilege review time by up to 75%.

- Demand for multilingual eDiscovery solutions is projected to increase by 200% between 2023 and 2028, driven by the growing volume of cross-border litigation, regulatory investigations, and international legal matters.

- Advanced neural machine translation technologies combined with legal-specific training are expected to achieve near-human translation accuracy by 2025, with error rates below 5% for major language pairs, improving the efficiency of multilingual document review and legal analysis.

Global eDiscovery Market Overview

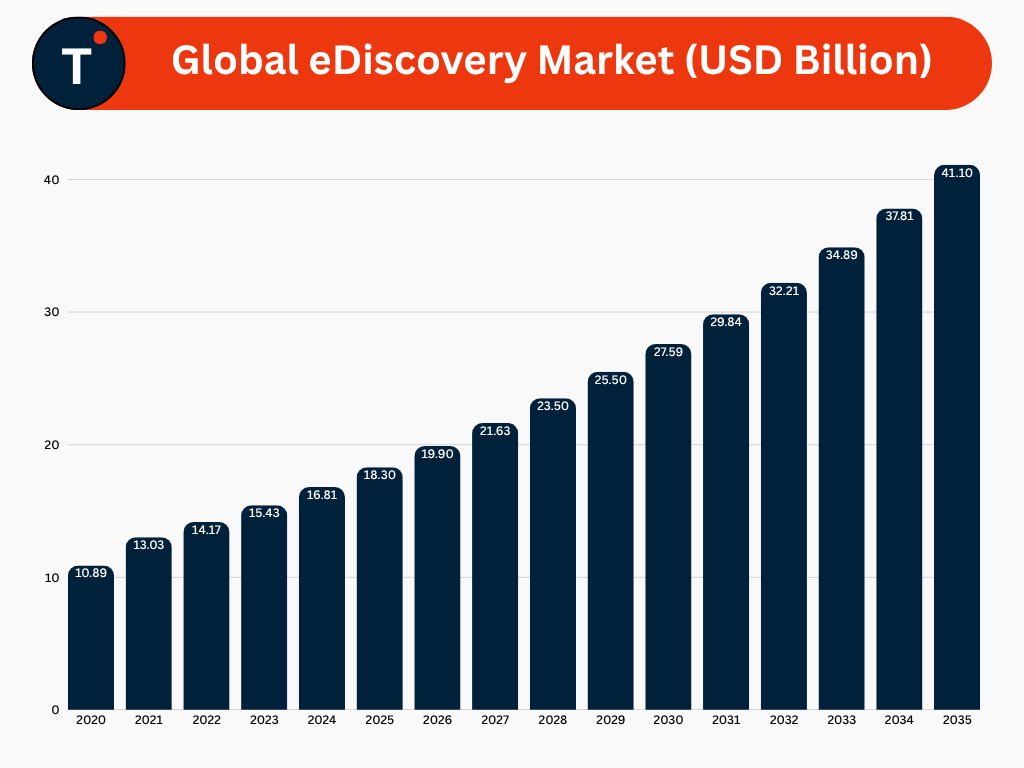

- The global eDiscovery market was valued at US$ 18.30 billion in 2025 and is projected to reach US$ 41.10 billion by 2035, reflecting a compound annual growth rate (CAGR) of 8.4% during the forecast period.

- Market growth is being driven by the increasing volume and complexity of electronically stored information (ESI), creating a greater need for efficient data identification, collection, and production processes.

- The expanding regulatory landscape and growing number of legal investigations, litigation matters, and compliance requirements continue to accelerate demand for eDiscovery solutions across industries.

- The adoption of advanced technologies, including artificial intelligence (AI), machine learning, predictive analytics, and cloud-based eDiscovery platforms, is enhancing review efficiency, improving accuracy, and reducing operational costs, further supporting market expansion.

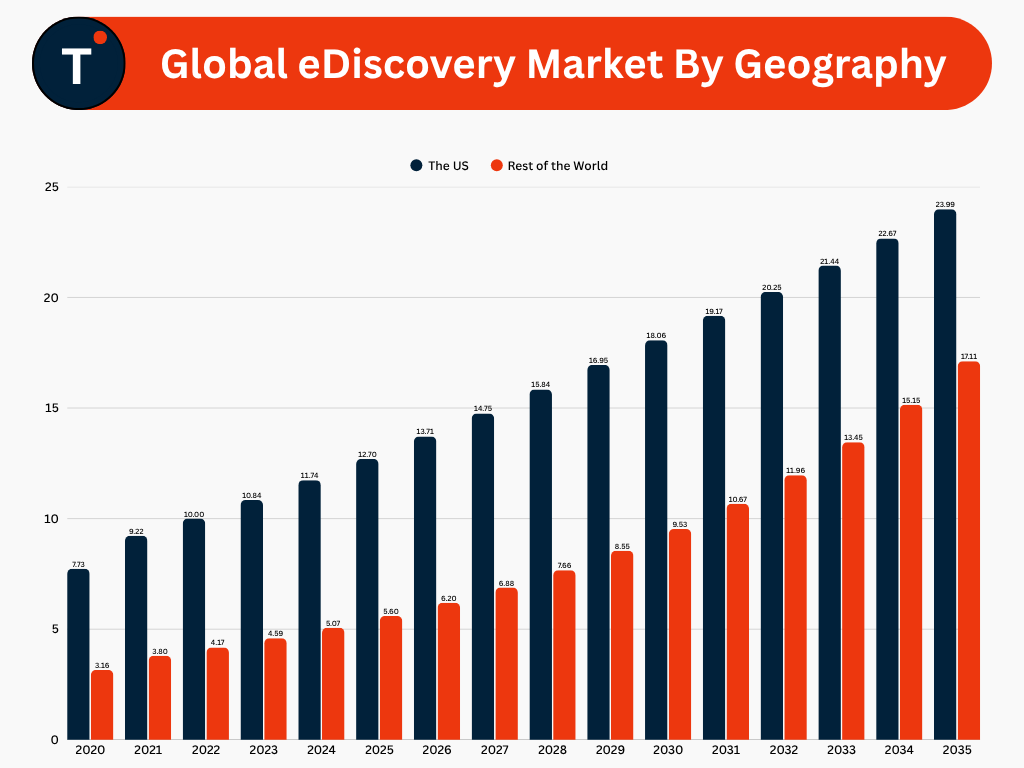

Global eDiscovery Market Geographical Overview

- The United States maintained its position as the largest contributor to the global eDiscovery market, accounting for 69.4% of total market revenue in 2025.

- The U.S. share of the global eDiscovery market is projected to decline to 58.4% by 2035, reflecting the increasing adoption of eDiscovery solutions across international markets and a more geographically diversified industry landscape.

- Despite the decline in market share, the U.S. eDiscovery market is expected to grow from US$ 12.70 billion in 2025 to US$ 23.99 billion by 2035, registering a CAGR of 6.4% during the forecast period.

- The Rest of the World (ROW) accounted for 30.6% of the global eDiscovery market in 2025 and is projected to increase its share to 41.6% by 2035.

- Growth in ROW markets is being driven by the globalization of legal services, increasing regulatory requirements, rising cross-border investigations, and expanding adoption of digital evidence management solutions.

- Spending across ROW markets is forecast to increase from US$ 5.60 billion in 2025 to US$ 17.11 billion by 2035, reflecting a CAGR of 11.9%, significantly outpacing growth in the U.S. market.

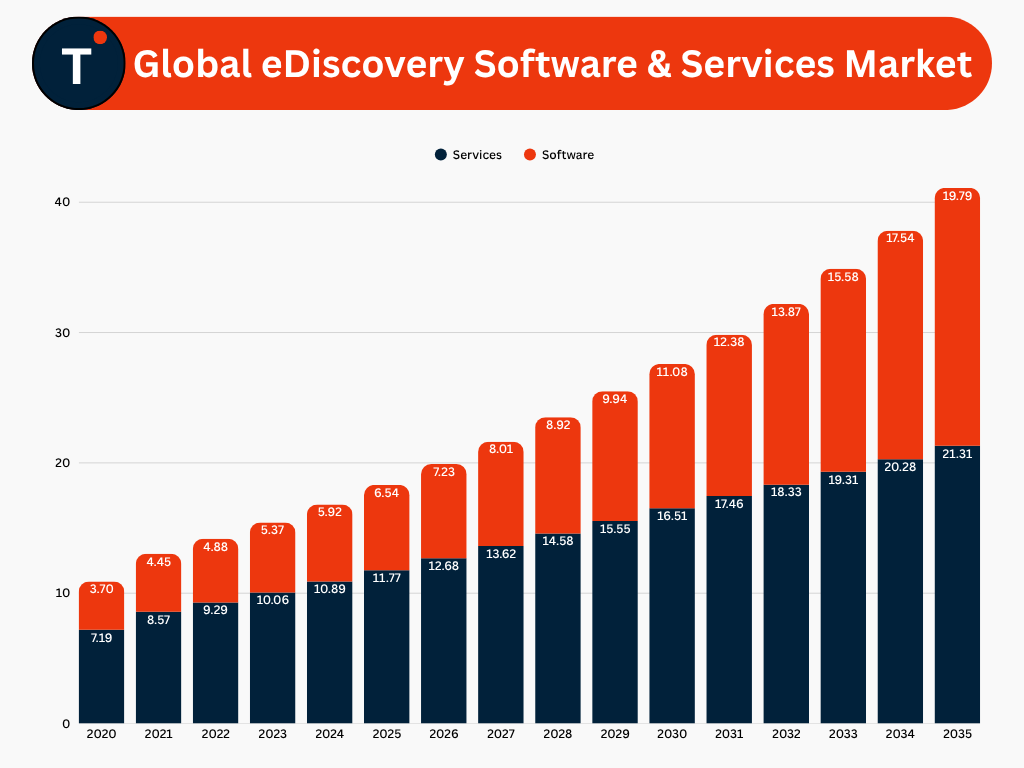

Global eDiscovery Software and Services Market Overview

- The services segment, which includes consulting, implementation, support, and managed services, is projected to grow from US$ 11.77 billion in 2025 to US$ 21.31 billion by 2035, registering a CAGR of 5.9% during the forecast period.

- The software segment is expected to expand at a CAGR of 11.8%, supported by growing adoption of advanced eDiscovery technologies and automation tools.

- Software spending is forecast to increase from US$6.54 billion in 2025 to US$19.79 billion by 2035, reflecting sustained investments in digital legal technologies.

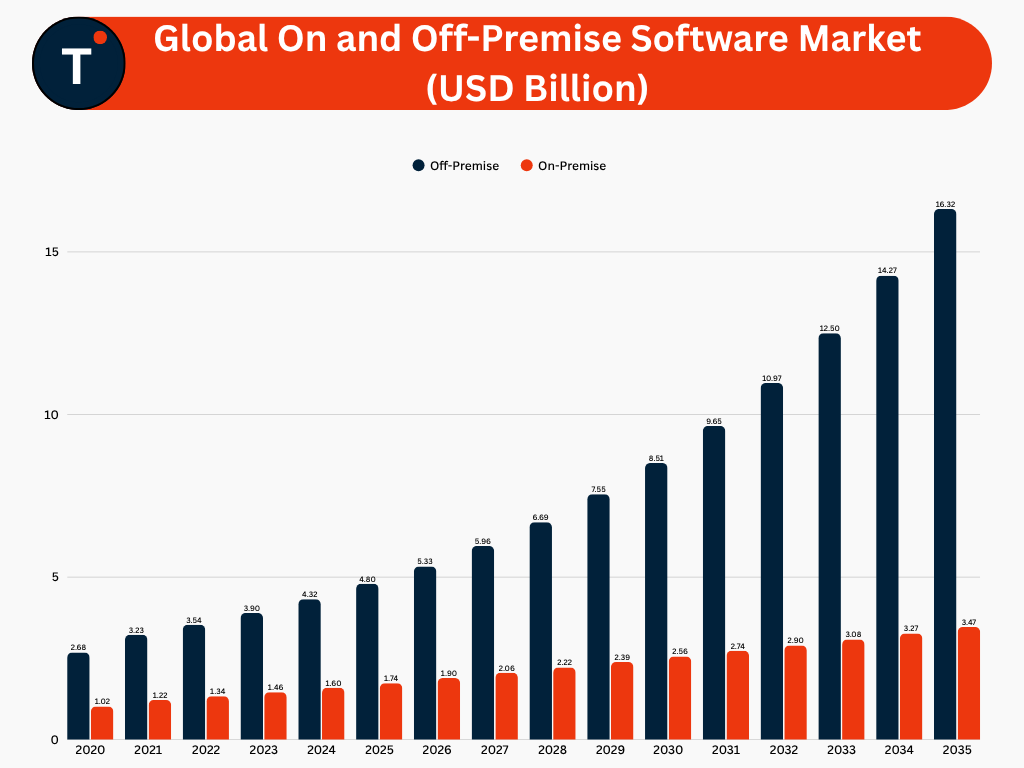

Global On and Off-Premise Software Market Overview

- The global eDiscovery market is experiencing a significant transition from traditional on-premise deployments to cloud-based, off-premise solutions, driven by increasing requirements for scalability, accessibility, flexibility, and operational efficiency.

- On-premise eDiscovery solutions accounted for 26.7% of the global market in 2025, representing US$1.74 billion in spending.

- The on-premise segment is projected to grow at a CAGR of 6.9% during the forecast period.

- Market share for on-premise solutions is expected to decline to 17.5% by 2035, despite spending increasing to US$3.47 billion, reflecting a gradual shift toward cloud-based deployment models.

- Off-premise eDiscovery solutions dominated the market, accounting for 73.3% of total market revenue in 2025, with spending reaching US$4.80 billion.

- The off-premise segment is anticipated to expand at a CAGR of 13.2%, significantly outpacing the growth of on-premise deployments.

- Market share for off-premise solutions is forecast to increase to 82.5% by 2035, demonstrating the growing preference for cloud-based eDiscovery platforms.

- Spending on off-premise eDiscovery solutions is expected to reach US$16.32 billion by 2035.

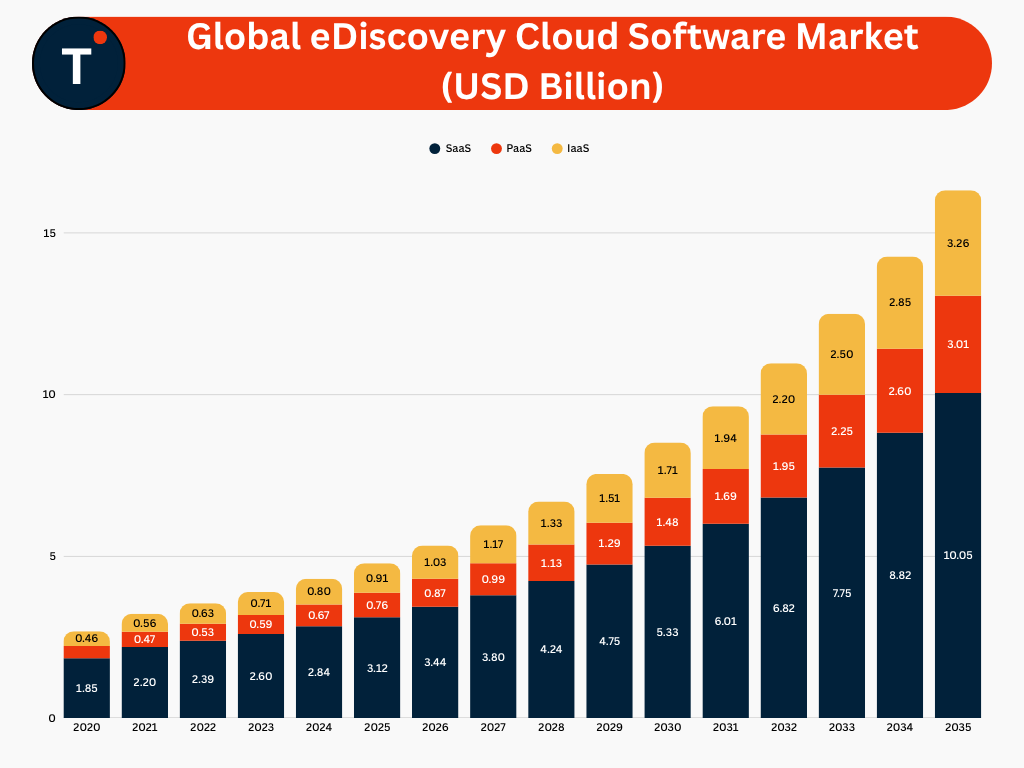

Global eDiscovery Cloud Software Market Overview

- The cloud software segment of the eDiscovery market, comprising Software as a Service (SaaS), Platform as a Service (PaaS), and Infrastructure as a Service (IaaS), continues to expand as organizations increasingly adopt cloud-based technologies to support eDiscovery operations.

- SaaS represented the largest share of the cloud eDiscovery software market, accounting for 65.1% of total off-premise spending in 2025.

- The SaaS segment is projected to maintain its leadership position, although its market share is expected to decline slightly to 61.6% by 2035 as adoption of other cloud service models accelerates.

- Spending on SaaS-based eDiscovery solutions is forecast to increase from US$3.12 billion in 2025 to US$10.05 billion by 2035, registering a CAGR of 12.7%.

- PaaS accounted for 15.9% of total cloud eDiscovery spending in 2025.

- The PaaS segment’s market share is expected to increase to 18.4% by 2035, reflecting growing demand for customizable cloud environments that support application development, integration, and advanced analytics capabilities.

- Spending on PaaS solutions is projected to grow from US$0.76 billion in 2025 to US$3.01 billion by 2035, achieving the highest growth rate among cloud deployment models with a CAGR of 14.8%.

- IaaS accounted for 19.0% of the cloud eDiscovery software market in 2025.

- The IaaS segment is projected to increase its market share to 20.0% by 2035, supported by growing demand for scalable storage, computing resources, and high-performance cloud infrastructure.

- Spending on IaaS solutions is expected to increase from US$0.91 billion in 2025 to US$3.26 billion by 2035, reflecting a CAGR of 13.6%.

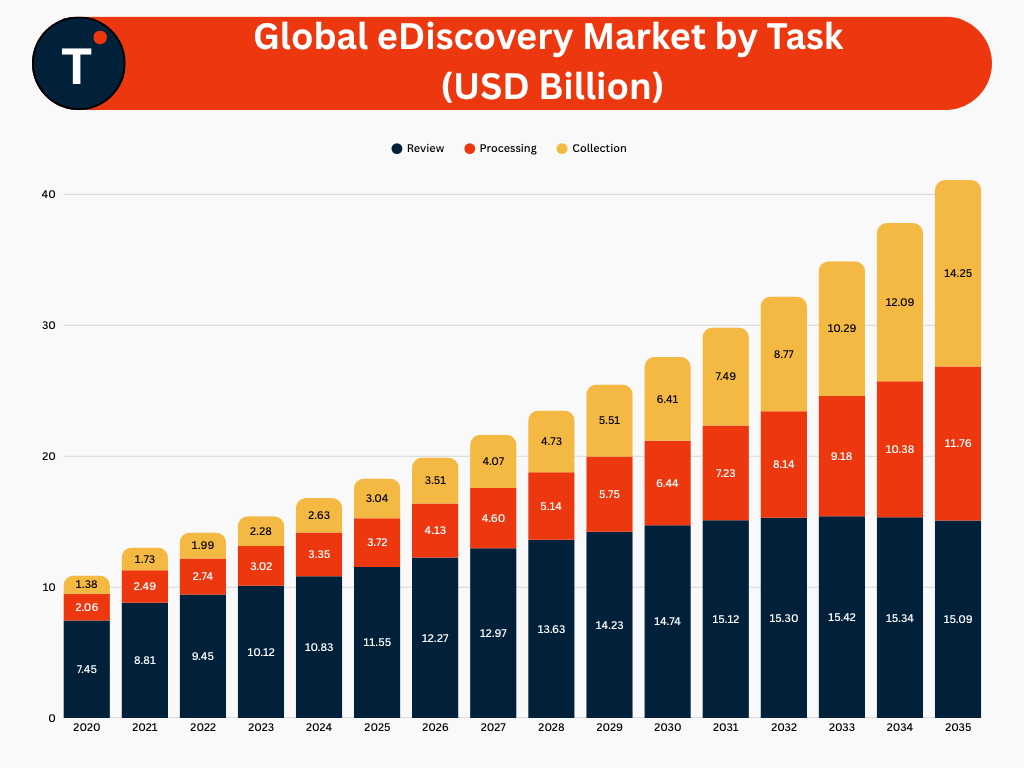

Global eDiscovery Market by Task Overview

- The review phase remained the largest component of the global eDiscovery market, accounting for 63.1% of total spending in 2025.

- Spending on review activities reached US$11.55 billion in 2025 and is projected to increase to US$15.09 billion by 2035.

- The share of review-related spending is expected to decline to 36.7% by 2035, reflecting the growing adoption of artificial intelligence, machine learning, and automation technologies that improve review efficiency and reduce manual workloads.

- The processing segment accounted for 20.3% of total eDiscovery spending in 2025, representing US$ 3.72 billion in market revenue.

- Spending on processing solutions is projected to increase to US$ 11.76 billion by 2035, driven by the growing volume, variety, and complexity of electronically stored information (ESI).

- The processing segment is expected to expand at a CAGR of 12.3% during the forecast period.

- Processing activities are anticipated to increase their share of the total market from 20.3% in 2025 to 28.6% by 2035, supported by rising demand for advanced analytics, data filtering, and automated workflow capabilities.

- The collection segment is projected to be the fastest-growing task category within the global eDiscovery market.

- The collection phase accounted for 16.6% of total market spending in 2025, representing US$ 3.04 billion in revenue.

- Spending on collection activities is expected to increase to US$ 14.25 billion by 2035, reflecting substantial growth in data preservation and acquisition requirements.

- The collection segment is forecast to register a CAGR of 16.8%, the highest among all eDiscovery task categories.

- Market share for collection activities is projected to increase from 16.6% in 2025 to 34.7% by 2035, driven by the expanding volume of digital evidence, increasing data sources, and growing regulatory requirements for comprehensive data collection.

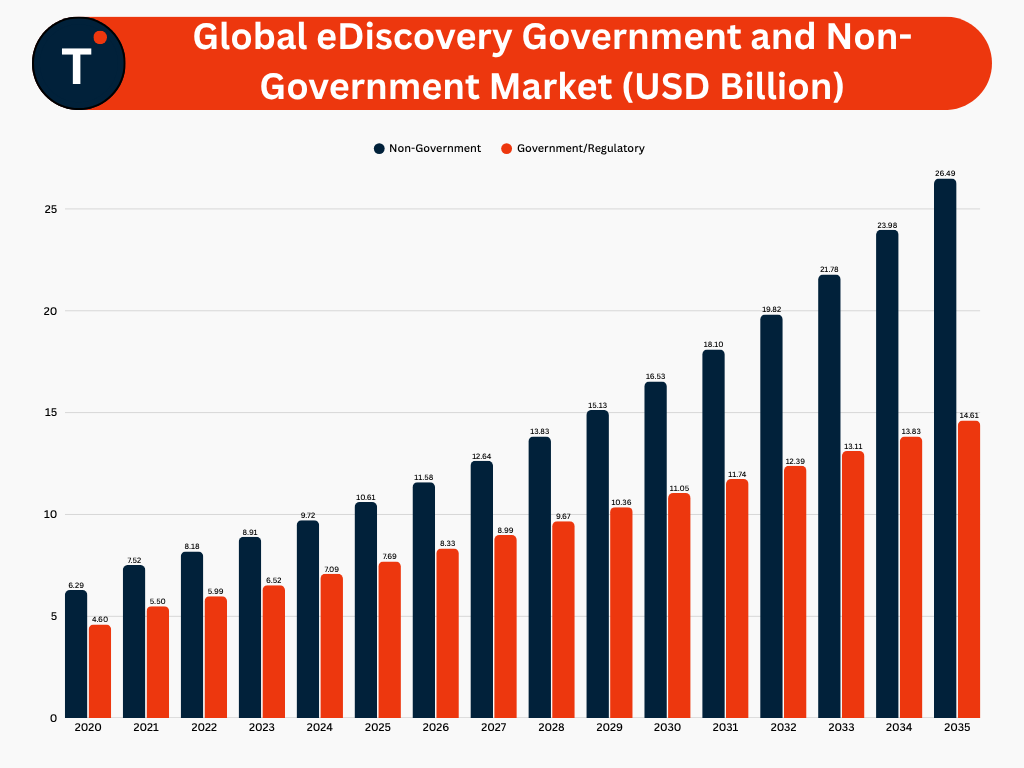

Global eDiscovery Government and Non-Government Market Overview

- The non-government segment, comprising corporate enterprises, law firms, and private sector organizations, represented 58.0% of the global eDiscovery market in 2025.

- The non-government segment is projected to increase its market share to 64.5% by 2035, reflecting growing adoption of eDiscovery solutions across commercial and private-sector organizations.

- Spending within the non-government segment is expected to increase from US$ 10.61 billion in 2025 to US$ 26.49 billion by 2035.

- The non-government segment is forecast to register a CAGR of 9.6%, making it the primary contributor to overall market growth during the forecast period.

- The government and regulatory segment accounted for 42.0% of the global eDiscovery market in 2025.

- The government and regulatory segment’s market share is projected to decline to 35.5% by 2035, reflecting faster growth within the private-sector segment.

- Despite the decline in proportional market share, spending in the government and regulatory segment is expected to increase from US$ 7.69 billion in 2025 to US$ 14.61 billion by 2035.

- The government and regulatory segment is anticipated to expand at a CAGR of 6.4% throughout the forecast period.

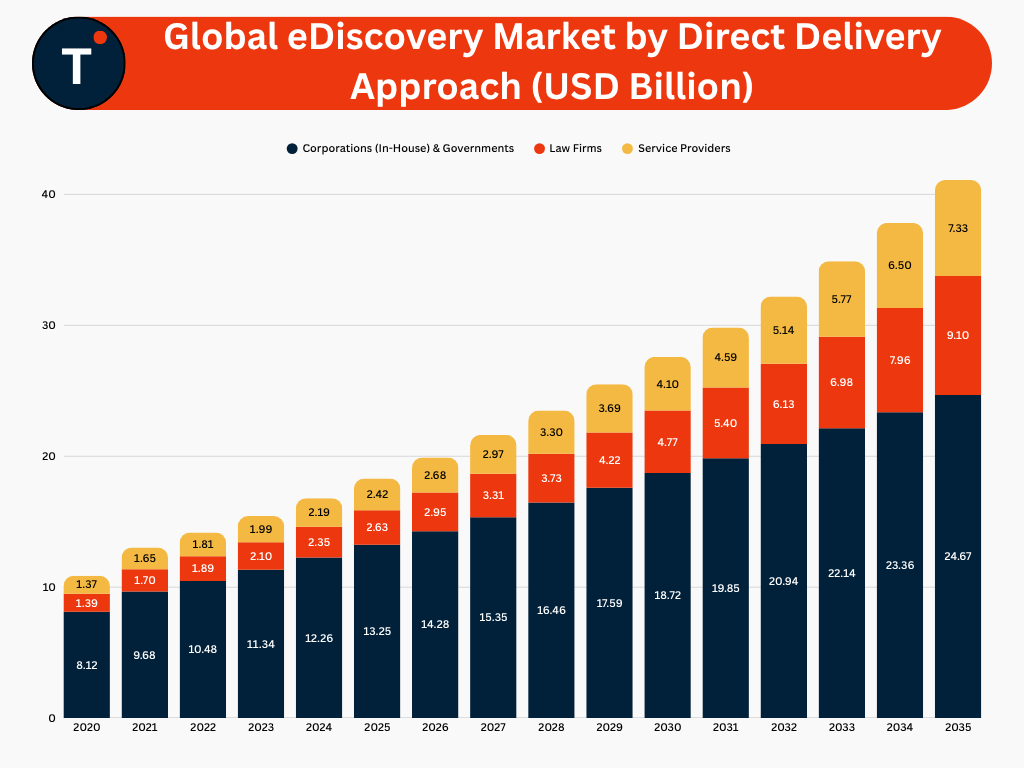

Global eDiscovery Market by Direct Delivery Approach

- Direct delivery in the eDiscovery market encompasses the execution of key tasks, including data collection, processing, and review, by corporations and government agencies, law firms, and third-party service providers.

- Corporations and government entities represented the largest delivery segment, accounting for 72.4% of total eDiscovery delivery spending in 2025.

- Spending within corporations and government segment reached US$ 13.25 billion in 2025.

- The corporations and government market share is projected to decline to 60.0% by 2035, reflecting the increasing involvement of external legal and service provider organizations.

- Despite the decline in market share, spending is expected to increase to US$ 24.67 billion by 2035, registering a CAGR of 6.3% during the forecast period.

- Law firms accounted for 14.4% of total eDiscovery delivery spending in 2025.

- The law firms market share is expected to increase to 22.1% by 2035, reflecting growing demand for specialized legal expertise and outsourced litigation support services.

- Spending by law firms is projected to increase from US$ 2.63 billion in 2025 to US$ 9.10 billion by 2035.

- The law firm segment is anticipated to expand at a CAGR of 13.3%, making it one of the fastest-growing delivery channels within the eDiscovery market.

- Third-party service providers represented 13.2% of the global eDiscovery delivery market in 2025.

- The segment’s market share is forecast to increase to 17.9% by 2035, driven by growing demand for managed eDiscovery services, advanced analytics, and specialized technology expertise.

- Spending on eDiscovery services delivered by external providers is expected to rise from US$ 2.42 billion in 2025 to US$ 7.33 billion by 2035.

- The service provider segment is projected to register a CAGR of 11.8%, supported by increasing outsourcing trends and the growing complexity of digital evidence management requirements.

Common Use Cases for eDiscovery in 2025

- Litigation was the leading eDiscovery use case, adopted by 95.7% of organizations.

- Investigations accounted for 82.0% of eDiscovery applications, making it the second-largest use case.

- Incident Response represented 50.7% of eDiscovery utilization, supporting cybersecurity and forensic investigations.

- Arbitration accounted for 48.6% of eDiscovery use cases, highlighting its importance in dispute resolution processes.

- Privacy Requests (DSARs) represented 46.4% of applications, driven by increasing data privacy regulations.

- Government Information Requests (FOIA) accounted for 43.5% of eDiscovery activities.

- HSR Second Requests for Mergers & Acquisitions represented 40.1% of eDiscovery use cases.

- Information Governance initiatives, including defensible deletion and ROT data removal, accounted for 35.6% of applications.

- Audits represented 32.0% of eDiscovery utilization across organizations.

Issues Impacting eDiscovery Business Performance

- Increasing Types of Data emerged as the leading challenge, cited by 24.59% of organizations, reflecting the growing diversity of electronically stored information (ESI).

- Increasing Volumes of Data accounted for 21.31% of reported challenges, highlighting the impact of rapid data growth on eDiscovery processes.

- Budgetary Constraints represented 19.67% of business performance challenges, limiting investments in advanced eDiscovery technologies and resources.

- Lack of Personnel was identified by 14.75% of organizations as a key challenge, underscoring the shortage of skilled eDiscovery professionals.

- Data Security Concerns accounted for 11.48% of reported issues, reflecting the importance of protecting sensitive and confidential information throughout the eDiscovery lifecycle.

- Inadequate Technology Infrastructure represented 8.20% of challenges, indicating the need for more advanced tools and platforms to support evolving eDiscovery requirements.

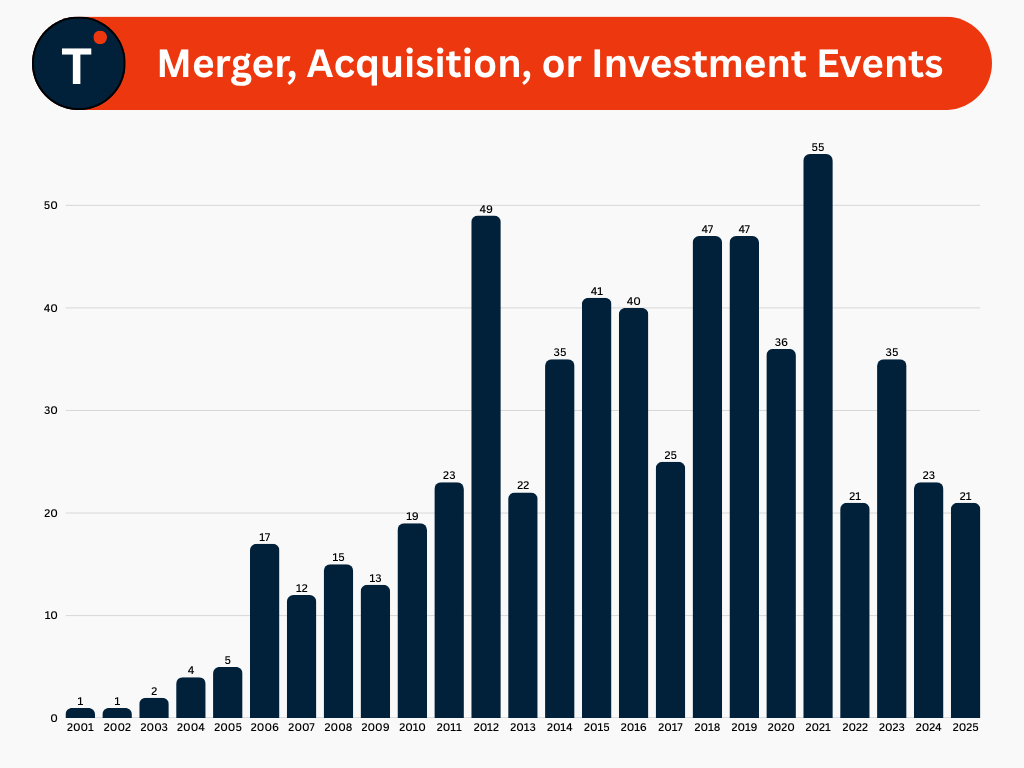

eDiscovery Mergers, Acquisitions, and Investments

- The eDiscovery market experienced limited merger, acquisition, and investment activity between 2001 and 2005, with annual transaction volumes remaining in the single digits as the industry remained in its early stages of development.

- Market consolidation accelerated from 2006 onward, reflecting increasing adoption of digital discovery technologies and the growing importance of electronically stored information (ESI) in legal and regulatory processes.

- 2012 represented a key milestone for the industry, recording 49 transactions and signaling a significant increase in investor and strategic acquisition activity.

- The market reached its highest level of activity in 2021, with 55 merger, acquisition, and investment transactions, driven by post-pandemic digital transformation initiatives, strong venture capital funding, and growing interest in AI-enabled legal technologies.

- Transaction activity declined significantly following the 2021 peak, falling to 21 deals in 2022, representing a 62% decrease year-over-year.

- The market experienced a partial recovery in 2023, with transaction volume increasing to 35 deals, before moderating to 23 transactions in 2024.

- The eDiscovery sector recorded 21 merger, acquisition, and investment transactions in 2025, matching the transaction volume reported in 2022.

- Deal activity in 2025 remained 62% below the 2021 peak, indicating a more selective investment environment focused on strategic acquisitions and targeted growth opportunities.

Conclusion

- The global eDiscovery market is expected to witness steady growth, driven by increasing volumes of digital data, evolving regulatory requirements, and growing adoption of AI-powered and cloud-based eDiscovery solutions.

- The United States remains the dominant contributor to the global eDiscovery market, supported by its mature legal ecosystem, high litigation activity, and early adoption of advanced legal technologies.

- Cloud-based deployments, predictive coding, and artificial intelligence are transforming eDiscovery workflows by improving efficiency, reducing costs, and enhancing review accuracy.

- Rising cross-border investigations, data privacy regulations, and digital evidence requirements are expected to create significant growth opportunities across global markets.

Add TriCityLocalNews as a Preferred Source on Google for instant updates!